The Ministry of Health (MOH) has announced that there will be IP rider changes in 2026. With these changes coming into effect, it helps to understand how IP riders work today and what these updates may mean for your household.

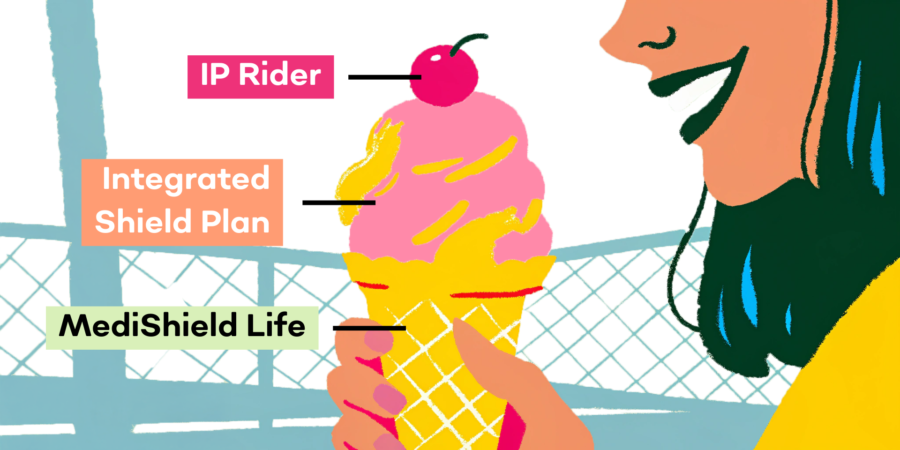

What is an Integrated Shield Plan (IP)

An Integrated Shield Plan (IP) is one of the ways Singaporeans strengthen their healthcare coverage beyond MediShield Life.

For many mothers, these plans are part of how they can prepare for medical situations that often arrive without warning, whether during pregnancy, early childhood, or later caregiving years.

What is IP Rider

An IP rider is an optional add-on to your Integrated Shield Plan that helps lower the amount you pay in cash when you are hospitalised.

It sits on top of MediShield Life and your IP, acting like a cushion to your fall that lessens the financial impact by reducing deductibles and co-payments. This can ease pressure during hospital stays, when families are often balancing care needs, work arrangements, and recovery at the same time.

How an IP Rider Works

Hospital coverage is layered in the following way:

1. MediShield Life

Basic national insurance for all Singaporeans that covers large hospital bills including:

• Hospital stays

• Surgeries

• Day surgeries

• Chemotherapy

• Radiotherapy

• Dialysis

2. Integrated Shield Plan (IP)

A private insurance upgrade that offers higher limits and access to private hospitals or higher ward classes.

3. IP Rider

An optional add-on that reduces your deductible and co-payment, so you pay less out of pocket.

Together, these layers determine how much financial support your family receives when medical care is needed.

Example of a Hospital Bill with and without an IP Rider

Below is a simplified illustration of how costs may differ.

Hospital bill: $30,000 (B2 ward)

| Item | MediShield Life Only | IP Without Rider | IP With Rider |

| Deductible | ~ $1,500 | ~$3,500 (depends on ward class) | Included in co-payment |

| Co-insurance/Co-payment | 10% after deductible = ~$2,850 | ~10% = $3,000 | ~5% = $1,500 |

| Claim limits | Subject to MediShield Life limits | Higher limits | Higher limits |

| Annual co-payment cap | Not applicable | Not applicable | E.g. $3,000 |

| Total out-of-pocket paid by you | ~$8,000 | ~$6,500 | ~$1,500 |

What Are the IP Rider Changes From 2026

On 26 November 2026, the MOH announced new requirements for IP riders that will take effect starting form 1 April 2026:

1. New riders can no longer cover the minimum deductible

New riders will not be allowed to cover the government-mandated IP deductible. This means policyholders must pay the deductible out of pocket before insurance payouts begin.

2. Co-payment cap will increase to minimum $6,000

The annual co-payment cap (previously $3,000) will be raised to a minimum of $6,000 per policy year. This cap applies to co-payments after the deductible has been paid.

3. Minimum 5% co-payment remains unchanged

Policyholders must continue to co-pay at least 5% of their hospital bill. Deductibles and co-payments can still be paid using MediSave, subject to prevailing withdrawal limits.

4. New riders are expected to be significantly cheaper

With reduced coverage, premiums for new private hospital riders are expected to be around 30 percent lower on average compared to existing riders that offered near-full coverage. This reflects a trade-off between lower monthly premiums and higher cost sharing when care is needed.

The aim is to preserve protection against catastrophic medical bills while making riders more sustainable in the long term.

Why the Ministry of Health Is Making These Changes

The Ministry has identified IP riders, especially those with near-full coverage, as a key driver of rising healthcare and insurance costs; particularly in the private sector. The reforms aim to:

• restore cost consciousness,

• moderate utilisation, and

• slow premium growth

while preserving protection against large medical bills.

What Does This Mean for People Who Already Have an IP Rider?

Existing riders are not immediately affected

Policyholders who purchased their IP rider before 27 November 2025 are not required to switch immediately. These riders can continue under existing terms even if they do not meet the new MOH requirements.

Over time, premium adjustments or plan migrations are likely as the market aligns with MOH’s sustainability objectives.

For riders purchased during the transition period

For riders purchased during the transition period (27 November 2025 to 31 March 2026), insurers are required to eventually transition policyholders to the new structure no later than 1 April 2028. Policyholders will be informed by their insurers ahead of time.

What Should Policyholders Do Now?

For those with existing IP riders, MOH and insurers advise against making rushed decisions. Instead:

• Review your renewal notices and insurer communications

• Understand how your deductible and co‑payment exposure may change in future

• Consider whether a lower‑premium, higher‑cost‑sharing model aligns with your cash flow and healthcare usage

Planning Ahead with Confidence

Insurance premiums rise with age. If coverage becomes unaffordable and lapses, families may be left without protection when health needs are higher.

For parents, planning is about balance. Choosing coverage that remains affordable over time helps protect both your family’s health and financial stability.

Healthcare planning is one of the quieter responsibilities many mothers carry, often in the background of daily life. By understanding how your coverage works today and what may change ahead, you can make informed choices that support your family with steadiness and confidence, both now and in the years to come.